2026 Credit Crunch: A Structural Threat Hidden in Market Complacency

- The ValueCritic

- Jun 21, 2025

- 6 min read

Despite tight high yield spreads and low default rates as of mid-2025, a historic test for credit markets is approaching. In 2026, over $500B in high yield bonds and leveraged loans must be refinanced, just as the two main funding engines, CLOs and private credit, are simultaneously showing signs of stress. This isn’t about credit quality, it’s about whether the plumbing of the leveraged finance system can absorb the surge in refinancing volume. With investor complacency still high and policy tools constrained, the stage is set for a potential credit repricing event.

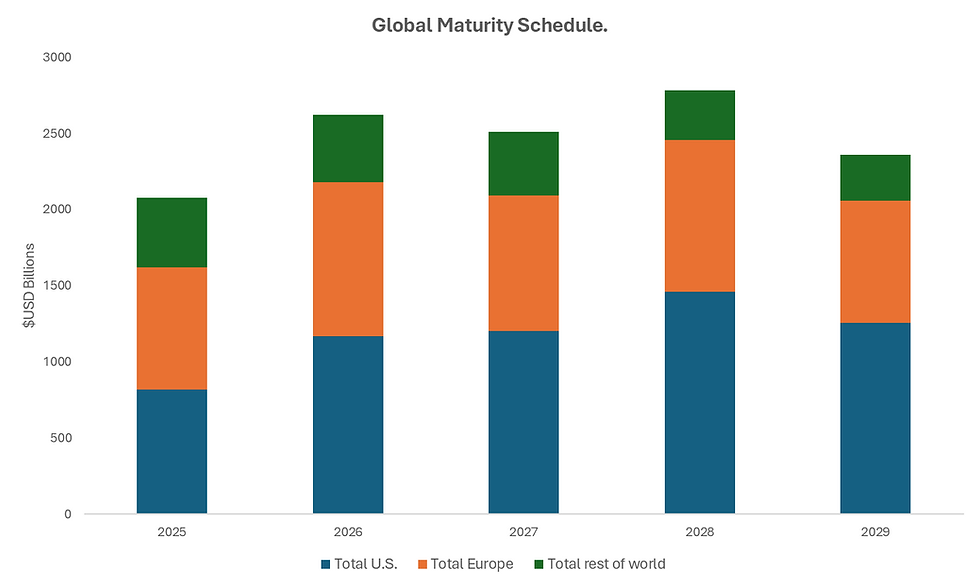

The Maturity Wall Explained.

Over $500 to 600B in high yield and leveraged loans are set to mature in 2026, the largest refinancing wave in decades. This debt was issued during 2020 to 2022, when interest rates were near zero. Companies locked in low coupons, typically around 5%, but will now face refinancing costs between 8 to10%. The problem isn't just the size of this wall, it's the timing. Roughly 50% of speculative-grade debt maturing between 2025 and 2028 is clustered in 2026. This creates a major capacity mismatch for lenders. In past cycles, maturities were more evenly spread. Now, everything hits at once. Worse, many borrowers issued debt assuming rates would stay low. Now, those with weak cash flows or high leverage face the prospect of default, debt restructuring, or expensive amend and extend deals.

For the Collateralized Loan Obligations (CLOs) market, which is the lifeblood of the leveraged loan market (historically purchasing about 60% of all newly issued loans) this engine is stalling at a critical moment.

Widening AAA Spreads: The top-rated (AAA) tranches of CLOs, the portion most investors buy have seen spreads widen from ~130 bps to over 200bps. This makes it more expensive to fund new CLOs.

Arbitrage Compression: A CLO earns money by capturing the difference between the yield on its loan assets and the cost of funding its tranches. That difference, or arbitrage, has narrowed significantly due to higher AAA funding costs and weaker loan spreads. With less room for profit, fewer deals make economic sense.

Equity Tranche Demand Is Falling: CLOs can't be issued unless someone buys the riskiest part the equity tranche. As equity investors become more cautious, fewer deals can get done, even if there's demand for AAA.

Basel III Endgame Headwinds: New capital rules are making it more expensive for banks and insurance companies to hold structured credit like CLOs. This reduces demand, particularly for the AAA tranches that used to be considered safe havens.

While 2024 broke records in total issuance, much of the volume came from resets and refinancing of existing deals. Net new CLO formation, critical to absorbing 2026 maturities, remains modest.Together, these constraints mean that CLO formation is grinding down just when the market needs it most. If CLOs don't roll, hundreds of billions in 2026 loan maturities won't have a buyer, putting the refinancing process at real risk.

Private credit, another key player in this market, saw a meteoric rise and has continued to reshaped corporate lending. But this growth masks a looming liquidity fragility just as the market leans on private capital to absorb 2026’s massive maturity wall.

The core problem lies in the structure of private credit funds, especially semi-liquid “evergreen” vehicles like Blackstone’s BCRED, Blue Owl’s OBDC, and Apollo’s ARCC. These vehicles promise investors periodic liquidity (monthly or quarterly redemptions), but the underlying loans are deeply illiquid and long-dated. That structural mismatch is now flashing red. Three dynamics are compounding:

Redemptions Are Climbing: Retail and institutional allocators have begun pulling capital. While most funds enforce monthly or quarterly gates (~2% NAV), cumulative redemption requests are exceeding thresholds. This forces managers to raise cash, either by selling assets or halting new loan origination.

NAVs Are Stale and Smooth: Private credit funds typically mark loans based on internal models, not observable market quotes. These models lag reality. During stress, fund NAVs can appear stable even as loan prices collapse in public markets. That illusion of stability is breaking down.

Liquidity Is Being Hoarded: In response to redemption pressure, managers are holding more cash, deferring new deployments, and avoiding new commitments, especially in riskier segments like subordinated debt or CLO equity. This is a stark reversal from 2020 to 2022, when private credit was the marginal buyer for risk.

The result, PC is stepping back just as refinancing needs peak. The very vehicles that were supposed to step in for banks and CLOs are turning inward, prioritizing fund survival over systemic liquidity provision.

A crucial but often overlooked early warning signal in credit markets is the Loan to Worst (LtW) ratio, the price of a leveraged loan relative to its projected recovery value in a worst-case scenario. In normal conditions, most loans trade between USD 97 and 99 cents on the dollar, reflecting healthy market confidence in repayment. But when refinancing risk rises, due to higher interest rates, tighter liquidity, or a slowdown in buyer demand, LtW prices begin to slip. Importantly, this shift can occur well before actual defaults rise or spreads widen, making LtW a leading indicator of structural stress rather than traditional credit deterioration.

In the context of 2026’s looming maturity wall, the LtW ratio becomes even more valuable. With over $500 to 600B in high yield and leveraged loans set to mature, borrowers will need to refinance in a vastly different environment than when their debt was issued. If market participants begin to doubt whether these borrowers can roll over their debt, especially those with weak free cash flow or high leverage, the LtW ratio will fall. This is not necessarily about creditworthiness deteriorating; it’s about market functionality breaking down.

Worryingly, LtW deterioration can create a feedback loop. As loans trade lower, investors demand wider spreads or avoid the primary market altogether. That, in turn, makes refinancing harder, pushing prices down further. In mid-2025, certain sectors, such as healthcare, software, and building products, are already seeing average LtW prices fall below 95 cents, suggesting the market is pricing in stress that has not yet shown up in official spread data or default rates.

Added to that, high yield borrowers are now facing borrowing costs around 7.5%, well above historical norms. Yet credit spreads remain tight, giving a false sense of calm. Why the disconnect? Because spreads only reflect credit risk, not the liquidity stress building beneath the surface.

This is a crucial oversight. Most investors use spreads to assess the chance of default but they don’t account for the difficulty of refinancing a huge wave of maturing debt. In 2026, over $500 to 600B in speculative-grade debt comes due. And while spreads look fine, effective yields are rising because Treasury rates are higher and demand from key lenders, CLOs and private credit, is fading.

If CLO issuance remains weak and private funds keep pulling back, refinancing will freeze. Only then will spreads start to widen, after the real damage is done. Put simply, the market is looking in the rearview mirror. Spreads are backward looking. Effective yields are forward looking. And the longer this gap holds, the more dangerously mispriced refinancing risk becomes.

So what does this mean for equity markets in 2026? If over $500B in high yield bonds and leveraged loans can’t be refinanced because CLOs and private credit funds are pulling back, many companies will face a serious cash crunch. They may have to restructure their debt, slash spending, or raise capital in ways that dilute shareholders. That could hurt earnings and confidence, especially in sectors already carrying high debt loads, or it could mean margins get further compressed if they have to refinance at a higher rate to entice investors for added levels of risk.

Meanwhile, the Federal Reserve has limited tools to prevent this kind of funding shock. Yes, it can cut interest rates, offer reassuring forward guidance, or revive emergency lending programs like PMCCF or TALF. But it can’t solve the root issues. The Fed doesn’t have the power to fix the shrinking demand for CLO equity, reverse the tougher Basel III bank rules, or stop investors from pulling money out of private credit funds. Even if the Fed cuts rates by 100 to150 bps, it might not make refinancing much easier unless loan market liquidity actually improves. While lower rates would help restore CLO economics and private credit flows, the Fed's own projections show most officials expect rates to stay near 4 to 3.5% through 2026. Unless spreads widen or issuance freezes, the Fed may not act preemptively, especially with inflation still above target. And even if they cut, they can’t fix structural problems like CLO equity shortages or private fund redemptions. That means policy relief may come too late to stop a liquidity-driven credit crunch.

The bottom line, the equity market may look calm heading into 2026, but credit markets are quietly flashing warning signs. If this funding squeeze worsens, stocks could suddenly reprice, not because of slowing growth or inflation, but because the credit plumbing underneath the system starts to fail.

Comments